While the legislature struggles with modifying Medicaid Expansion, costing more, getting less insured, Governor Brad Little on the campaign trail was beating a different drum. He was looking beyond the twisted shorts condition of legislative Republicans who fought Proposition 2; he can see the bigger picture. Health insurance for those beyond Idaho’s exchange, Your Health Idaho, are getting squeezed out of health care insurance.

To be eligible for participation in the exchange you have to make between 100%-400% of the federal poverty level. Medicaid expansion addresses those below 138% FPL.

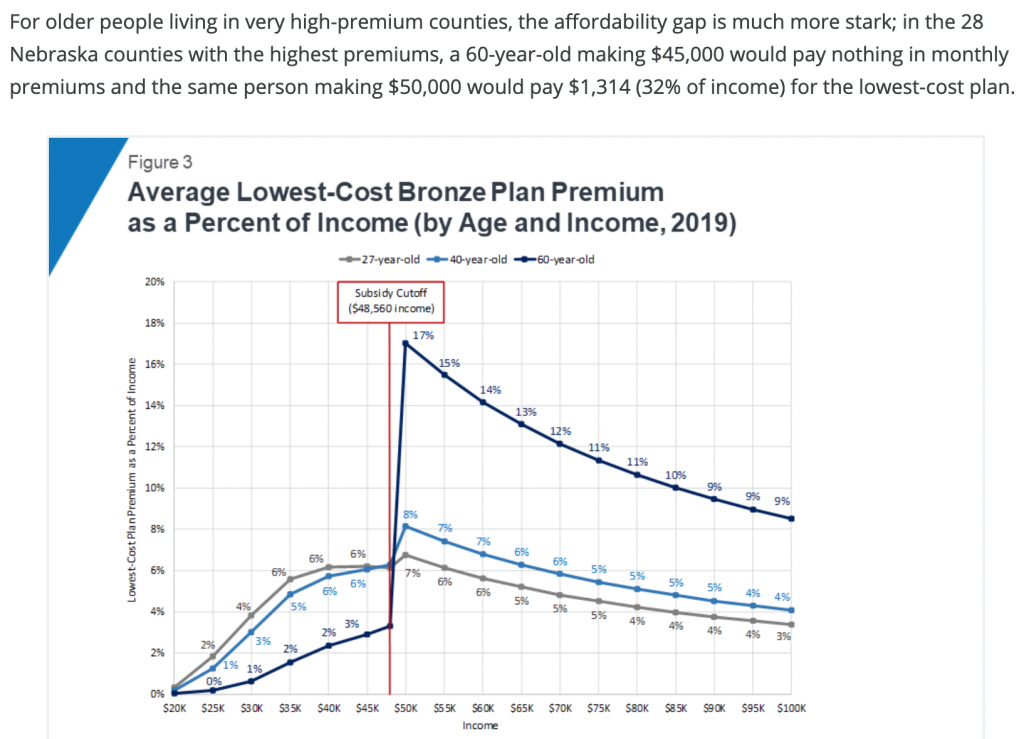

If you are a 60-year-old and you can participate on the YHI exchange and you make $45K per year, you might only have to pay 3% of your income for health insurance since you get subsidies. But if you make more than the 400% upper limit to participate in YHI, say up to $50K, you wouldn’t be eligible for exchange subsidies and the cost might jump to 32% of your income. This is called the health insurance “subsidy cliff”. Many Idahoans are standing on it. That’s me folks. And it’s steep. Why would I pay a fifth to a third of my income for something I might not use? I’d be a fool. Most Idahoans aren’t.

This is where the growing numbers for Idaho’s Catastrophic Health Plan are coming from. There is “the gap” population, the 70,000 below the 100% limit for enrollment on YHI, who will now be covered by expanded Medicaid; they won’t be the uninsured anymore. But those above 400% are going to or have dropped health insurance because they aren’t fools. Brad pointed this out whenever he could. I didn’t hear his solution.

The trouble with Idaho’s indigent program is, we take your assets if you can’t pay your medical bills. The really low-income folks, those below 100% often had few assets. But I imagine those making $50K have some tools, a work truck, maybe a back hoe the county can file a lien on. There goes their health and their means of income if they get unlucky and sick. Welcome to Idaho and medical bankruptcy.

So, beyond Bernie’s “Medicare for All”, what can Idaho do about this? It’s a head scratcher. Brad keeps talking about the Idaho High Risk Pool model and it’s worth consideration. The HRP was developed 20 years ago by State Senator Dean Cameron (now Director of the Department of Insurance) for people with preexisting conditions who couldn’t get health insurance. It was funded by a tax on all other health insurances sold in the state. It worked well for the ten years before the ACA eliminated preexisting conditions as an exclusion, then the enrollment dwindled to double digits and the fund ballooned to $20M. Could such a plan work again?

Some states have tried it, the reinsurance model, but each has varying success based on how much cost they are willing to shift. That’s the key, the willingness to properly fund the investment.

It’s worth fixing this. Most businesses in Idaho have less than 50 employees. There are many small shops or self-employed folks who drive this economy and need this support to make health insurance affordable.

A recent suggestion from the Trump administration was for states to apply for waivers to Medicaid to allow subsidies for those above 400%. Of course, for this to fit the budget neutral requirement, the subsidies for lower income folks would have to go down to pay for the higher income folks cost reductions. Isn’t that how it always goes?

Polls show most people are not happy with how health insurance works in this country. Why can’t Idaho take some time and effort and make this work for our citizens? It’s worth the effort.